Rising Home Prices Mean Great News for Homeowners

Recently there has been a lot of talk about home prices and if they are accelerating too quickly. As we mentioned before,

in some areas of the country, seller supply (homes for sale) cannot

keep up with the number of buyers who are out looking for homes, which

has caused prices to rise.

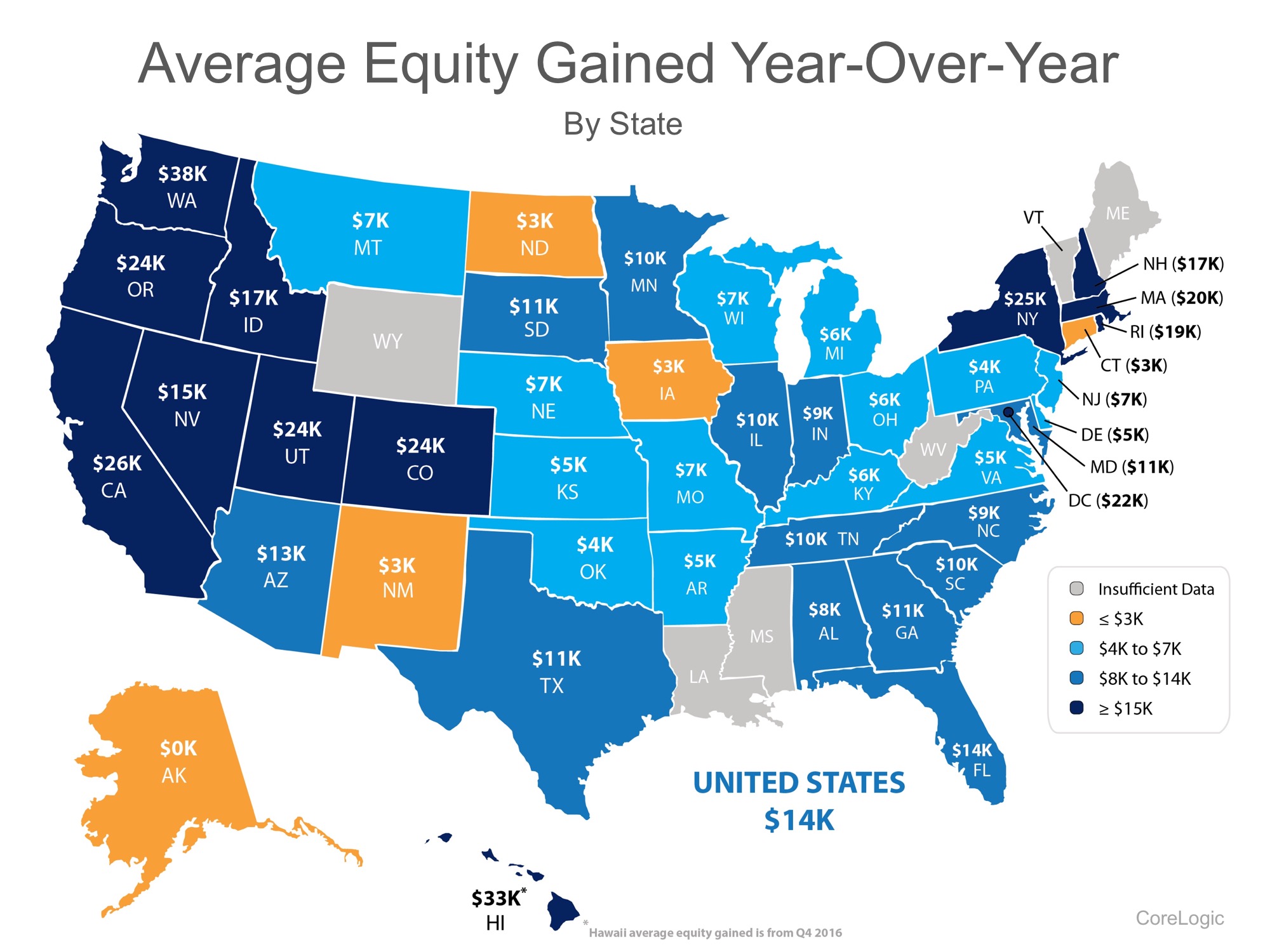

The great news about rising prices, however, is that according to CoreLogic’s Homeowner Equity Report, the average American household gained over $14,000 in equity over the course of the last year, largely due to home value increases.

The map below was created using the same report from CoreLogic and shows the average equity gain per mortgaged home during the 1st quarter of 2017 (the latest data available).

For those who are worried that we are doomed to repeat 2006 all over again, it is important to note that homeowners are investing their new-found equity in their homes and themselves, not in depreciating assets.

The added equity is helping families put their children through college, invest in starting small businesses, pay off their mortgages sooner and even move up to the home that will better suit their needs now.

The great news about rising prices, however, is that according to CoreLogic’s Homeowner Equity Report, the average American household gained over $14,000 in equity over the course of the last year, largely due to home value increases.

The map below was created using the same report from CoreLogic and shows the average equity gain per mortgaged home during the 1st quarter of 2017 (the latest data available).

For those who are worried that we are doomed to repeat 2006 all over again, it is important to note that homeowners are investing their new-found equity in their homes and themselves, not in depreciating assets.

The added equity is helping families put their children through college, invest in starting small businesses, pay off their mortgages sooner and even move up to the home that will better suit their needs now.

![Home Buying Myths Slayed [INFOGRAPHIC] | MyKCM](https://d8yi0qr1xsq5x.cloudfront.net/2017/07/11143516/Slaying-Myths-STM-1046x1477.jpg)

![The Cost of Renting vs. Buying in the US [INFOGRAPHIC] | MyKCM](https://d8yi0qr1xsq5x.cloudfront.net/2017/06/20140414/20170623-Rent-vs.-Buy-STM-1046x1354.jpg)