Click on photo below for interior pictures

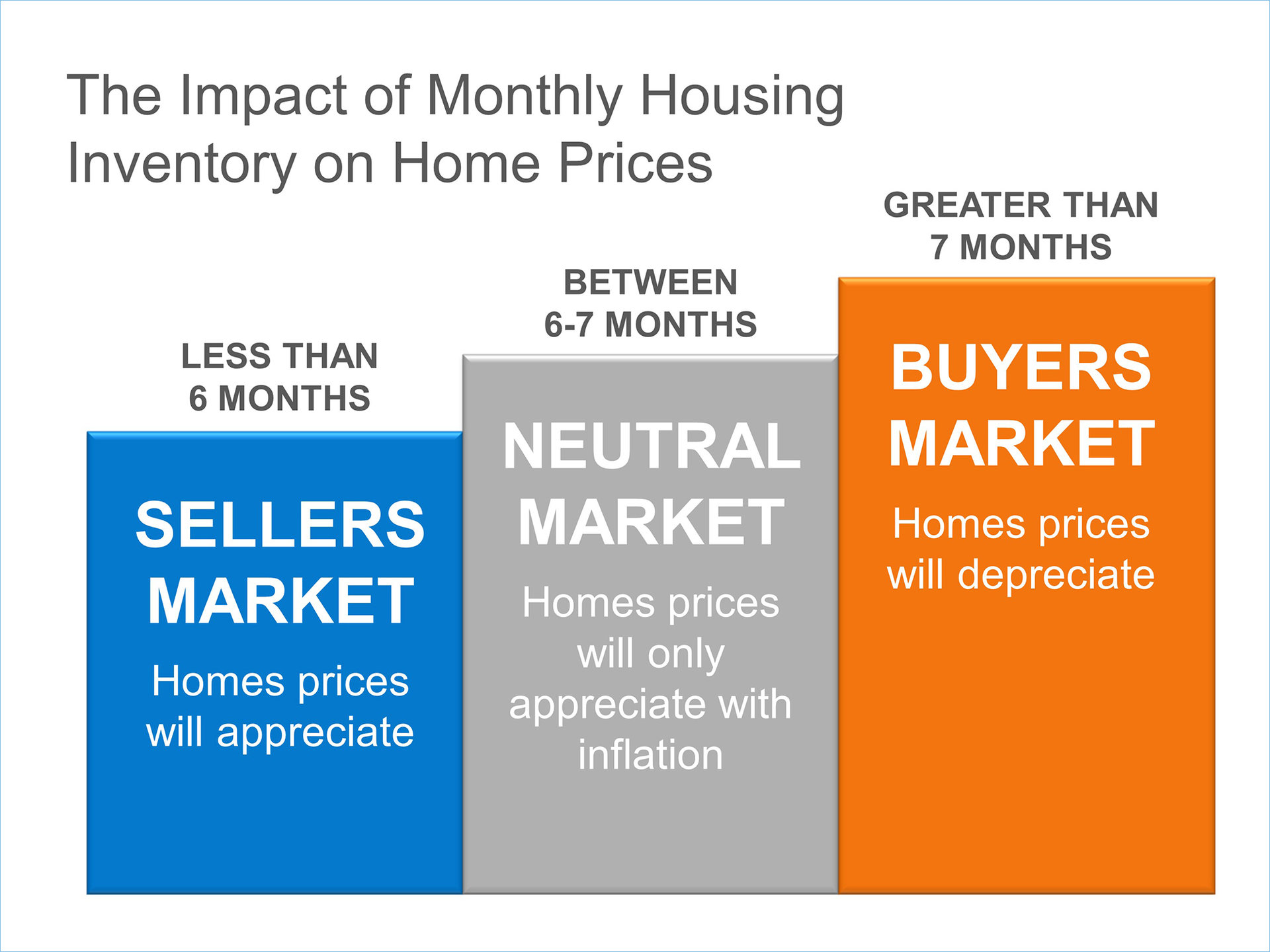

The price of any item is determined by the supply of that item, and

the market demand. The National Association of Realtors (NAR) recently

released their latest Existing Home Sales Report.

The price of any item is determined by the supply of that item, and

the market demand. The National Association of Realtors (NAR) recently

released their latest Existing Home Sales Report.

"Limited inventory amidst strong demand continues to push home prices higher, leading to declining affordability for prospective buyers."NAR’s President, Chris Polychron added:

"The demand for buying has really heated up this summer, leading to multiple bidders and homes selling at or above asking price."

![Cost Across Time [INFOGRAPHIC] | Keeping Current Matters](http://www.keepingcurrentmatters.com/wp-content/uploads/2015/07/20150724-Cost-Across-Time-KCM.jpg)

“Households must consume housing whether they own or rent. Not even accounting for more favorable tax treatment of owning, homeowners pay debt service to pay down their own principal while households that rent pay down the principal of a landlord plus a rate of return.Christina Boyle, a Senior Vice President, Head of Single-Family Sales & Relationship Management at Freddie Mac, explains another benefit of securing a mortgage vs. paying rent:

That’s yet another reason owning often does—as Americans intuit—end up making more financial sense than renting.”

“With a 30-year fixed rate mortgage, you’ll have the certainty & stability of knowing what your mortgage payment will be for the next 30 years – unlike rents which will continue to rise over the next three decades.”As an owner, your mortgage payment is a form of ‘forced savings’ which allows you to have equity in your home that you can tap into later in life. As a renter, you guarantee the landlord is the person with that equity.

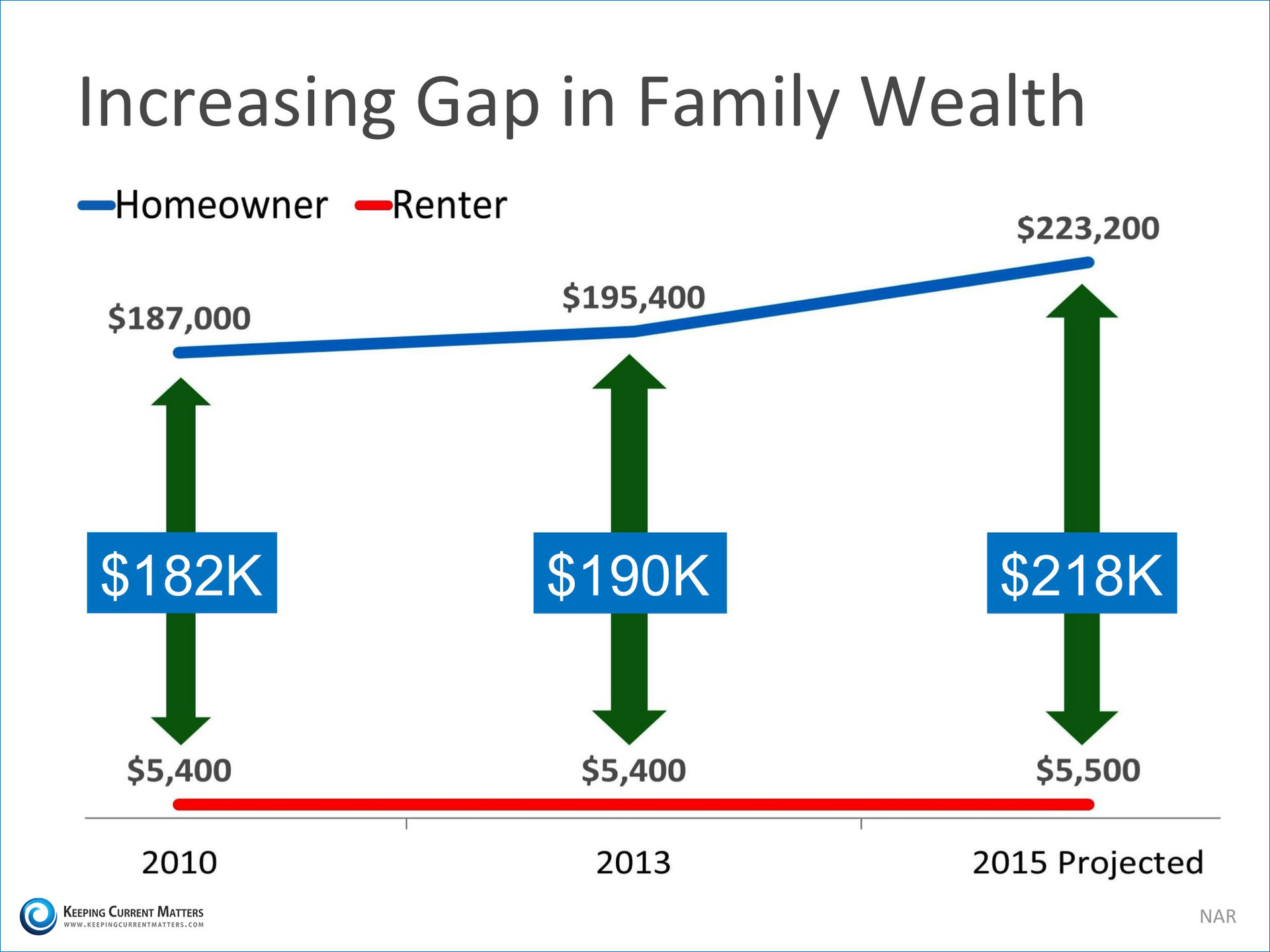

“Over the past quarter century the largest single source of wealth for all but the richest households nearing retirement age has been their homes, which accounted for about two-fifths of net worth in the early 1990s and accounts for about one-third today.”2. Home equity is a very important source of net worth to all but the wealthiest households near retirement age.

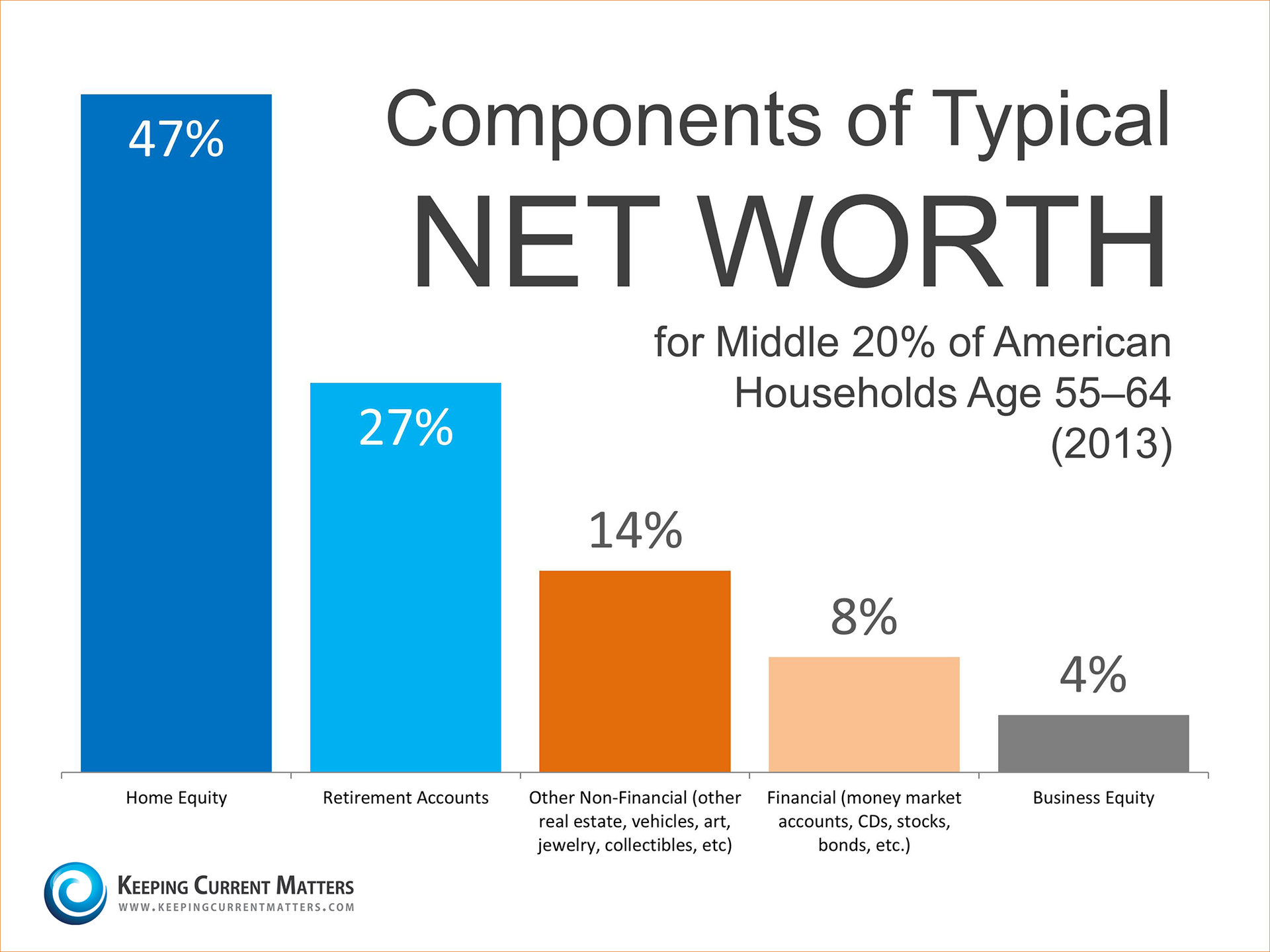

“Home equity is an important source of wealth for middle income households, accounting for more than one-third of total net worth for the second, third, and fourth quintiles of the net worth distribution… The fifth quintile has a much larger share in business equity—almost a quarter—than any other quintile. (The figure leaves out the bottom quintile of households because they have negative net worth. It is likely that these households will rely almost exclusively on Social Security in retirement.)”Here is an asset breakdown for the middle 20% of Americans determined by median net worth ($165, 720):

![Boomerang Buyers Coming Back in Force [INFOGRAPHIC] | Keeping Current Matters](http://www.keepingcurrentmatters.com/wp-content/uploads/2015/07/Boomerang-KCM.jpg)